Social Security is not disappearing, but latest report shows Congress still faces hard choices

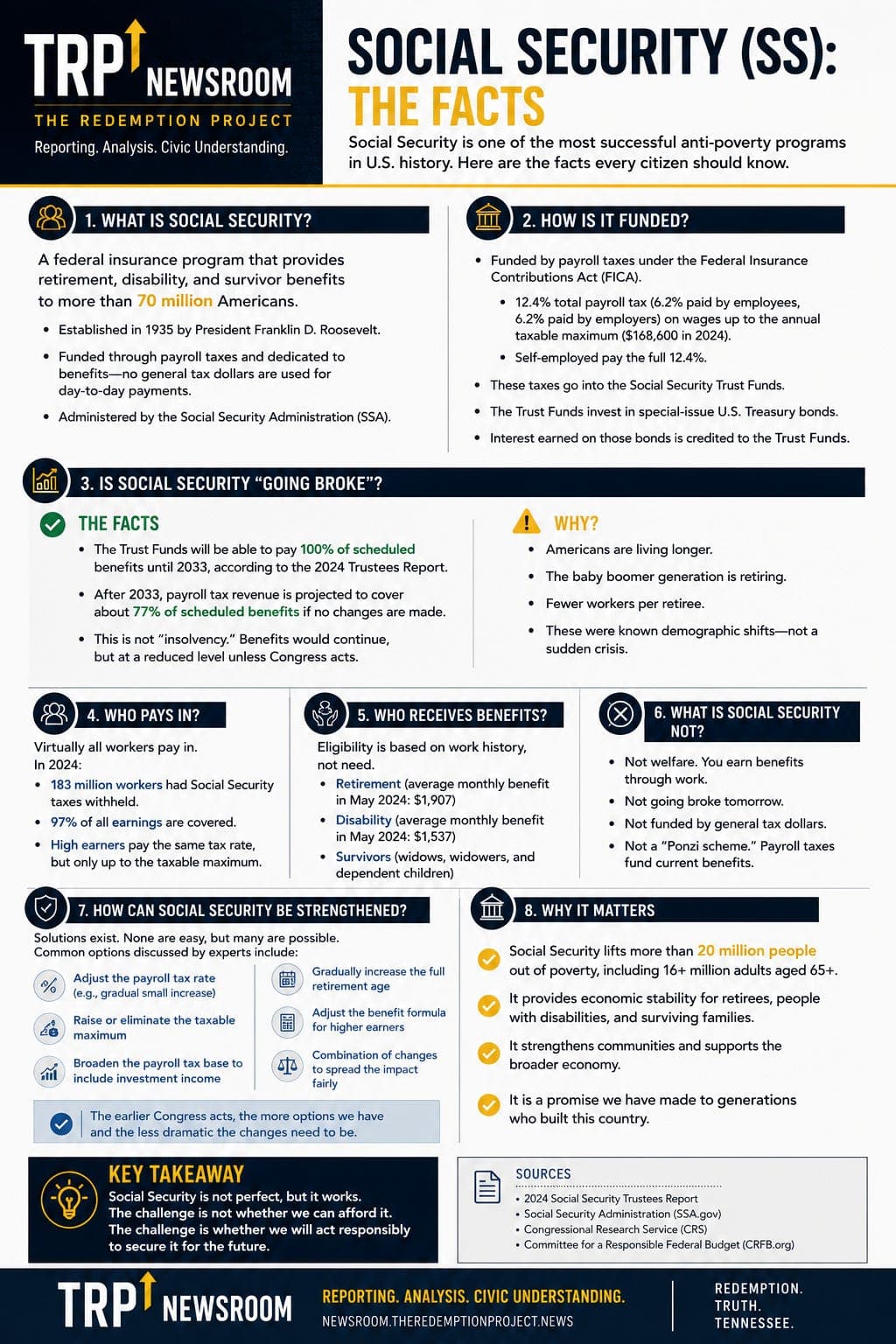

by Brandon Burley and The Redemption Project WASHINGTON — Social Security is not projected to disappear, but the program’s latest financial report shows the nation’s largest retirement and disability insurance system is still on a path that would leave it unable to pay full scheduled benefits without action from Congress. The 2026 annual report from the Social Security trustees projects that the combined reserves of the Old-Age and Survivors Insurance and Disability Insurance trust funds would be depleted in the third quarter of 2034 if the two funds were considered together. At that point, continuing program income would be enough to pay 83 percent of scheduled benefits, according to the trustees. That distinction matters. Trust fund depletion does not mean Social Security stops sending checks. It means that, under current law, the program would no longer have enough trust fund reserves and incoming revenue to pay full scheduled benefits on time. Social Security is funded largely through payroll taxes paid by workers and employers. Those taxes would continue to come in even after trust fund reserves are depleted. The issue is whether that continuing revenue would be enough to cover the full benefit promises written into law. The trustees say it would not. The program is often discussed as one system, but it is financed through two legally separate trust funds. The Old-Age and Survivors Insurance Trust Fund pays retirement and survivor benefits. The Disability Insurance Trust Fund pays disability benefits. Those funds cannot actually be combined unless Congress changes the law. Still, the trustees often show a combined projection to give a broader picture of Social Security’s overall financial condition. The retirement and survivor fund faces the earlier shortfall. The trustees project the Old-Age and Survivors Insurance Trust Fund will be able to pay full scheduled benefits until the fourth quarter of 2032. After that, continuing income would be sufficient to pay 78 percent of scheduled benefits. The Disability Insurance Trust Fund is in stronger condition. The trustees project it will be able to pay full scheduled benefits through at least 2100, the final year of the report’s long-range projection period. Put simply, Social Security’s disability side is not the immediate problem. The larger pressure is on the retirement and survivor side, where costs are rising faster than dedicated income. The trustees reported that, at the end of 2025, 62.3 million people received retirement or survivor benefits and 8.2 million people received disability benefits. About 184.7 million people paid Social Security payroll taxes in 2025. The two Social Security trust funds together ended 2025 with about $2.56 trillion in reserves. But costs exceeded income by about $160.2 billion that year, continuing a trend in which reserves are being drawn down to help pay current benefits. The trustees estimate Social Security’s 75-year actuarial deficit at 4.42 percent of taxable payroll. That is worse than the 3.82 percent estimate in the prior year’s report. An actuarial deficit is not the same thing as immediate bankruptcy. It is a measure of how far projected income falls short of projected costs over the long term. The program’s financing challenge is driven by several factors, including population aging, lower fertility assumptions, slower labor force growth and the relationship between the number of workers paying into the system and the number of beneficiaries receiving payments. The trustees also noted that recent tax legislation is expected to reduce future revenue from income taxes on Social Security benefits. Social Security taxes are paid on wages up to an annual taxable maximum. For 2026, that taxable maximum is $184,500. Employees and employers each pay 6.2 percent for Social Security, while self-employed workers pay the combined 12.4 percent rate. Beneficiaries also received a 2.8 percent cost-of-living adjustment for 2026, according to the Social Security Administration. Cost-of-living adjustments are designed to help benefits keep pace with inflation, but they do not solve the program’s long-term financing gap. A separate June analysis from the Penn Wharton Budget Model reached a similar conclusion, though with slightly different dates and percentages. Penn Wharton projected that if the retirement and disability funds were treated together, the combined fund would be depleted in February 2035. At that point, 86 percent of scheduled benefits would be payable. Penn Wharton estimated that closing its projected 75-year shortfall would require raising the combined employer-employee payroll tax rate from 12.4 percent to 17.1 percent, reducing benefits by an equivalent amount, or using some combination of tax increases and benefit changes. The trustees do not recommend one specific solution. Their report says lawmakers have many options and that taking action sooner would allow a broader range of choices and more time to phase in changes. Congress could increase payroll tax revenue, change the taxable wage cap, adjust benefit formulas, change retirement-age rules, use general revenue or combine several approaches. Subscribe now Each option comes with tradeoffs. Raising payroll taxes would bring in more money but would increase the tax burden on workers, employers or both. Raising or eliminating the taxable wage cap would collect more revenue from higher earners but would change how the tax burden is distributed. Reducing scheduled benefits would lower costs but affect retirees, survivors, people with disabilities or future beneficiaries, depending on how changes are designed. Changing the retirement age could reduce long-term costs, but it would also affect workers differently depending on health, occupation and life expectancy. Using general revenue could protect scheduled benefits, but it would move Social Security further away from its traditional dedicated-financing structure. Doing nothing is also a policy choice. If Congress makes no changes, the trustees project that current law would eventually require benefits to be limited to the amount payable from continuing income once reserves are depleted. Social Security cannot borrow to pay benefits beyond available program income and trust fund reserves. That is why headlines saying Social Security is “going broke” can mislead the public. The program is not projected to vanish. But headlines saying there is “nothing to worry about” are also incomplete. The more accurate explanation is that Social Security would continue to collect revenue and pay benefits, but scheduled benefits would not be fully payable under current law after trust fund reserves are depleted. The civic question is not whether Social Security will exist. The question is whether Congress will act before the shortfall arrives, how large the changes will need to be and who will bear the cost. For current retirees, near-retirees, younger workers and future taxpayers, timing matters. Changes made earlier can be phased in over time. Changes made later tend to be more abrupt because there is less time to spread the cost across workers, beneficiaries and generations. Social Security remains one of the most important federal programs in American life. It provides retirement, survivor and disability benefits to tens of millions of people and is funded by payroll contributions from nearly the entire working population. That size is exactly why the math matters. The latest report does not say Social Security is ending. It says the program’s current financing structure does not support full scheduled benefits indefinitely. Congress has tools to address that gap. The unresolved question is whether lawmakers will use them before the trust fund deadline forces a more painful debate. I am a retired detective and criminal justice / government educator based in Tennessee. I am a commentary write for Tennessee Lookout and a weekly columnist with Knox TN Today . My work examines public policy, public safety systems and civic responsibility. My reporting and commentary have also appeared in Governing , The Arizona Capitol Times , South Florida Sun Sentinel , Police1 , among other state and regional outlets. Subscribe now

See an error? Request a correction